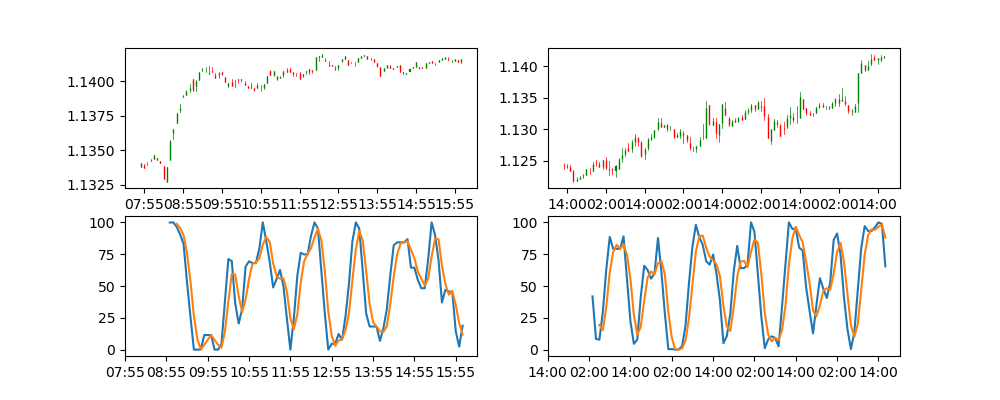

この記事では、1分足から5分足と1時間足のローソク足チャートを作成し、

その下にそれぞれのDTオシレーターを表示するスクリプトを作成します。

1分足の取得

今後GymのEnvに使っていきたいので、足を取得する部分は以前作ったEnvをそのまま使用します。

余計なことも書いてあるので適宜無視してください。

ただし、EnvではdropしていたOpenの値は必要になるので残すように変更しておきます。

ローソク足の作成、表示

mpl_financeを使用してローソク足チャートを表示します。

ポイント

xticksに日付時刻をそのまま使用してしまうと休日などで時刻のギャップが空いた際にチャートも空白になってしまうので、

xtickにはダミーの連番を用います。

dummy_indices_5m = np.linspace(0, len(target_5m), len(target_5m))

そして、xticklabelsに日付時刻を使用することで表示上は日付時刻が表示されます。

# DTOは1つ減るのでtickを合わせるため1始まり

x_tick = [i for i in np.array(indices_5m.to_pydatetime())][1::12]

x_tick_labels_5m = [i.strftime('%H:%M') for i in x_tick]

ax.set(xticks=dummy_indices_5m[1::12], xticklabels=x_tick_labels_5m)

DTOの作成、表示

DTOを作成します。

今回のパラメータは

period_rsi = 8

period_stoch = 5

period_sk = 3

period_sd = 3

で作成します。

RSIの計算

RSIの計算方法は色々なサイトに載っているのでそれを参考にしてください。

$$ \rm{RSI} = 100 – \frac{100}{1 + \rm{RS}} $$

# RSI計算(8)

close = target_5m['close']

diff = close.diff()[1:]

up, down = diff.copy(), diff.copy()

up[up < 0] = 0

down[down > 0] = 0

up_sma = up.rolling(window=8, center=False).mean()

down_sma = down.abs().rolling(window=8, center=False).mean()

rs = up_sma / down_sma

rsi = 100.0 - (100.0 / (1.0 + rs))

DTOの計算

DTOはストキャスティクスRSIを平滑化させたものなので、そのように作成します。

(参考:DT オシレーターのソースを読み解く)

# DTOの計算

rolling = rsi.rolling(period_stoch)

llv = rolling.min()

hhv = rolling.max()

sto_rsi = 100 * ((rsi - llv) / (hhv - llv))

sk = sto_rsi.rolling(period_sk).mean()

sd = sk.rolling(period_sd).mean()

結果

ソース全文

from random import random

import numpy as np

import os

from builtins import range, print

from builtins import Exception

import datetime

import pandas

from dateutil import relativedelta

import matplotlib.pyplot as plt

import mpl_finance as mpf

class FxDtoEnv:

def __init__(self):

# 観測できる足数

self.visible_bar = 100

# CSVファイルのパス配列(最低4ヶ月分を昇順で)

self.csv_file_paths = []

now = datetime.datetime.now()

for _ in range(4):

now = now - relativedelta.relativedelta(months=1)

filename = 'DAT_MT_EURUSD_M1_{}.csv'.format(now.strftime('%Y%m'))

if not os.path.exists(filename):

print('ヒストリーファイルが存在していません。下記からダウンロードしてください。', filename)

print('http://www.histdata.com/download-free-forex-historical-data/?/metatrader/1-minute-bar-quotes/EURUSD/')

raise Exception('ヒストリーファイルが存在していません。')

else:

self.csv_file_paths.append(filename)

self.data = pandas.DataFrame()

for path in self.csv_file_paths:

csv = pandas.read_csv(path,

names=['date', 'time', 'open', 'high', 'low', 'close', 'v'],

parse_dates={'datetime': ['date', 'time']},

dtype={'datetime': np.long, 'open': np.float32, 'high': np.float32, 'low': np.float32, 'close': np.float32}

)

csv.index = csv['datetime']

csv['datetime'] = csv['datetime'].astype(np.long)

# ohlcを作る際には必要

# csv = csv.drop('datetime', axis=1)

# csv = csv.drop('open', axis=1)

# histdata.comはvolumeデータが0なのでdrop

csv = csv.drop('v', axis=1)

self.data = self.data.append(csv)

# 最後に読んだCSVのインデックスを開始インデックスとする

self.read_index = len(self.data) - len(csv)

self.read_index = int(random() * len(self.data))

self.tickets = []

def make_obs(self, mode):

"""

5分足、1時間足の2時系列データをvisible_bar本分作成する

:return:

"""

target = self.data.iloc[self.read_index - 60 * env.visible_bar: self.read_index]

if mode == 'human':

m5 = np.array(target.resample('5min').agg({'high': 'max',

'low': 'min',

'close': 'last'}).dropna().iloc[-1 * self.visible_bar:][target.columns])

h1 = np.array(target.resample('1H').agg({'high': 'max',

'low': 'min',

'close': 'last'}).dropna().iloc[-1 * self.visible_bar:][target.columns])

return np.array([m5, h1])

elif mode == 'ohlc_array':

m5 = np.array(target.resample('5min').agg({'high': 'max',

'low': 'min',

'close': 'last'}).dropna().iloc[-1 * self.visible_bar:][target.columns])

h1 = np.array(target.resample('1H').agg({'high': 'max',

'low': 'min',

'close': 'last'}).dropna().iloc[-1 * self.visible_bar:][target.columns])

return np.array([m5, h1])

period_rsi = 8

period_stoch = 5

period_sk = 3

period_sd = 3

env = FxDtoEnv()

target = env.data.iloc[env.read_index - 60 * env.visible_bar: env.read_index]

# humanの場合はmatplotlibでチャートのimgを作成する?

fig = plt.figure(figsize=(10, 4))

# ローソク足は全横幅の太さが1である。表示する足数で割ってさらにその1/3の太さにする

width = 1.0 / env.visible_bar / 3

# 5分足

ax = plt.subplot(2, 2, 1)

# y軸のオフセット表示を無効にする。

ax.get_yaxis().get_major_formatter().set_useOffset(False)

target_5m = target['close'].resample('5min').ohlc().dropna().iloc[-1 * env.visible_bar:]

indices_5m = target_5m.index

dummy_indices_5m = np.linspace(0, len(target_5m), len(target_5m))

data_5m = pandas.DataFrame({'datetime': dummy_indices_5m,

'open': target_5m['open'],

'high': target_5m['high'],

'low': target_5m['low'],

'close': target_5m['close']}).values

mpf.candlestick_ohlc(ax, data_5m, width=width, colorup='g', colordown='r')

# DTOは1つ減るのでtickを合わせるため1始まり

x_tick = [i for i in np.array(indices_5m.to_pydatetime())][1::12]

x_tick_labels_5m = [i.strftime('%H:%M') for i in x_tick]

ax.set(xticks=dummy_indices_5m[1::12], xticklabels=x_tick_labels_5m)

# DTO(8,5,3,3)

ax = plt.subplot(2, 2, 3)

# RSI計算(8)

close = target_5m['close']

diff = close.diff()[1:]

up, down = diff.copy(), diff.copy()

up[up < 0] = 0

down[down > 0] = 0

up_sma = up.rolling(window=8, center=False).mean()

down_sma = down.abs().rolling(window=8, center=False).mean()

rs = up_sma / down_sma

rsi = 100.0 - (100.0 / (1.0 + rs))

# DTOの計算

rolling = rsi.rolling(period_stoch)

llv = rolling.min()

hhv = rolling.max()

sto_rsi = 100 * ((rsi - llv) / (hhv - llv))

sk = sto_rsi.rolling(period_sk).mean()

sd = sk.rolling(period_sd).mean()

dto_indices_5m = sk.index

dummy_indices_dto_5m = np.linspace(0, len(dto_indices_5m), len(dto_indices_5m))

ax.plot(dummy_indices_dto_5m, sk, label="sk")

ax.plot(dummy_indices_dto_5m, sd, label="sd")

x_tick = [i for i in np.array(dto_indices_5m.to_pydatetime())][::12]

x_tick_labels_dto_5m = [i.strftime('%H:%M') for i in x_tick]

ax.set(xticks=dummy_indices_dto_5m[::12], xticklabels=x_tick_labels_dto_5m)

# 1時間足

ax = plt.subplot(2, 2, 2)

# y軸のオフセット表示を無効にする。

ax.get_yaxis().get_major_formatter().set_useOffset(False)

target_1h = target['close'].resample('1H').ohlc().dropna().iloc[-1 * env.visible_bar:]

indices_1h = target_1h.index

dummy_indices_1h = np.linspace(0, len(target_1h), len(target_1h))

data_1h = pandas.DataFrame({'datetime': dummy_indices_1h,

'open': target_1h['open'],

'high': target_1h['high'],

'low': target_1h['low'],

'close': target_1h['close']}).values

mpf.candlestick_ohlc(ax, data_1h, width=width, colorup='g', colordown='r')

# DTOは1つ減るのでtickを合わせるため1始まり

x_tick = [i for i in np.array(indices_1h.to_pydatetime())][1::12]

x_tick_labels_1h = [i.strftime('%H:%M') for i in x_tick]

ax.set(xticks=dummy_indices_1h[1::12], xticklabels=x_tick_labels_1h)

# DTO(8,5,3,3)

ax = plt.subplot(2, 2, 4)

# RSI計算(8)

close = target_1h['close']

diff = close.diff()[1:]

up, down = diff.copy(), diff.copy()

up[up < 0] = 0

down[down > 0] = 0

up_sma = up.rolling(window=8, center=False).mean()

down_sma = down.abs().rolling(window=8, center=False).mean()

rs = up_sma / down_sma

rsi = 100.0 - (100.0 / (1.0 + rs))

# DTOの計算

rolling = rsi.rolling(period_stoch)

llv = rolling.min()

hhv = rolling.max()

sto_rsi = 100 * ((rsi - llv) / (hhv - llv))

sk = sto_rsi.rolling(period_sk).mean()

sd = sk.rolling(period_sd).mean()

dto_indices_1h = sk.index

dummy_indices_dto_1h = np.linspace(0, len(dto_indices_1h), len(dto_indices_1h))

ax.plot(dummy_indices_dto_1h, sk, label="sk")

ax.plot(dummy_indices_dto_1h, sd, label="sd")

x_tick = [i for i in np.array(dto_indices_1h.to_pydatetime())][::12]

x_tick_labels_dto_1h = [i.strftime('%H:%M') for i in x_tick]

ax.set(xticks=dummy_indices_dto_1h[::12], xticklabels=x_tick_labels_dto_1h)

plt.show()

コメント